The preference for home ownership appears deeply ingrained as evidenced by people’s fascination with the latest house price movements, the myriad of home renovation shows on TV and even in the usage of acronyms such as ‘FOMO’ to describe our anxiety around making that all important home purchase.

However, this quest for homeownership may have come at a cost. Australia’s household debt to disposable income ratio has risen sharply over the past decade to almost 200% and despite the cooling of the housing market in recent years, significant barriers to entry persist, particularly for younger Australians.

We need to ask ourselves several questions, such as:

For how much longer can we rely on structural changes such as interest rate cuts and increasing workplace participation to drive house prices upward?

Interest rates are approaching zero, meaning for many, principal repayments already represent about the same value as their interest payments. But are historically low interest rates the new normal? And if not, how will Australian households cope with higher interest burdens?

The labour force has been boosted considerably by greater workforce participation by women, which now stands at 60.7%, just 10.2% less than men. But will the higher share of women currently employed part-time compared to men translate to higher levels of full-time female employment in the future to further support rising household incomes?

Could we in fact be in for some negative structural changes?

Australia’s ageing population will see the workplace having to prop up the elderly to a greater extent, which is likely to place further pressures on household finances. How will already financially constrained households respond to this challenge and how will this impact upon the type of demand for housing?

Is a large proportion of the wealth created through housing more a product of forced saving rather than smart investment?

Finally, most people are not good savers, so does owning a home simply constitute a way of forced saving?

With the above points in mind, perhaps now is the time to question whether the dream of home ownership is one worth still aspiring to, and whether it is time to let go of the oft-quoted mantra that ‘rent money is dead money.’ What if rather than purchasing, you rented your accommodation and invested the money saved by not owning property in other assets classes? How would such a strategy compare to buying? In this article we focus upon the apartment market and take a retrospective approach to compare the net financial position (or payoff) that would result under each of the following strategies:

Details regarding our methodology, which to a degree follows that of a 2013 paper by Crowley and Li are provided below:

Put simply, the payoff to buyers is defined as the benefits of buying (i.e. price appreciation), less the initial (one-off) costs of buying, less the ongoing ownership costs.

The payoff to renters is defined as the benefits of renting less the initial (one-off) and ongoing costs of renting.

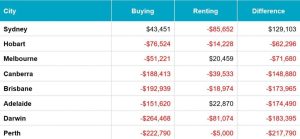

Figure 1 summarises the payoffs under the respective buying and renting/investing strategies for each of the state and territory capital cities.

Our results indicate that over the last ten-year holding period, Sydney is the only city in which the payoff to purchasers is positive. By contrast, those who purchased in other cities lose out in comparison to those who rent.

This means that Sydney is the only city in which it is optimal to have bought in December 2009 with the net payoff of $43,451 being $129,103 higher than the -$85,652 net payoff to Sydney renters.

The superior result achieved by those who purchased in Sydney reflects the fact that this city recorded the highest rate of capital growth of 5.6% p.a. over the ten-year study period.

Melbourne and Hobart ranked second and third with growth of 4.1% and 3.6% respectively. Consequently, purchasers in these cities are closer to breaking even compared to those in the remaining state and territory capitals.

However, apart from Sydney, the average annual capital growth recorded by all capital cities over the ten years stood below the average standard variable rate of 4.7% p.a. payable by purchasers on their mortgages. This in conjunction with the other ongoing costs associated with property ownership means that the net financial position of buyers in these cities remains further in the red at the end of the ten-year holding period.

Whilst the payoff to renters in most cities is also negative, the lower initial and ongoing costs associated with renting in tandem with the returns earned on the savings invested in the share market and term deposits (which averaged 3.2% and 3.5% p.a. respectively over the ten-years), means that the net financial position of renters in all cities, except Sydney, is superior. In fact, the differential between the two strategies is above $150,000 for five of the state/territory capitals.

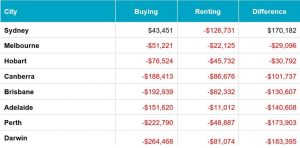

One potential limitation of our analysis (and other studies that seek to assess the rent versus buy decision) relates to the fact that the median sales value and median rent data are based upon different properties with different characteristics and quality. As such, a comparison of median prices with median rents at any point in time is likely to reflect quality differences between owner occupier and rental stock (the implicit assumption being that owner-occupier properties may well be of a higher standard).

To account in some way for these differences, we have rerun the rental analysis with a 10% rental premium each year. The results of which are presented below (for convenience the net payoff to buyers is also presented):

It is evident from the above table that the increased rental cost over the holding period is insufficient to change the optimal strategy to purchasing in any of the cities that our earlier analysis identified as favouring renters.

The higher rental cost does, of course, reduce the outperformance of the renting and investing payoff in these cities. Repeating the analysis with a 20% rental premium, yields a similar result.

It seems that even after adjusting for perceived differences in quality between owner and rented stock, a strategy of renting and investing would have proved optimal for those deciding whether to buy or rent in December 2009 in all Australian state and territory capital cities, except Sydney.

The outperformance of the rent and invest strategy in most cities may be counter-intuitive to what most people would expect. Arguably, the results found here may change over different periods of time and holding period durations. Nonetheless, it is a stark reminder that buying may not always be the best option and assuming (and this, indeed, is a big assumption) that renters have the discipline to invest the money that they save by not purchasing, then perhaps a viable alternative to home ownership does indeed exist.

The Australian rental market, however, currently carries a high risk to the tenant with respect to their longevity of tenure and potentially this is a large contributor towards people’s desire to own their own home. By contrast, America’s build-to-rent market has strong security of tenure, whereby a tenant can continue to roll their rental year upon year without risk of the landlord terminating their lease. Could an increase in build-to-rent product in Australia see more people move to this form of residence, potentially making high financial gains through prudent saving and investing outside of residential property?

As financiers of all manner of property transactions nationally Dorado is interested in understanding the performance of different strategies in different markets and felt that this article may raise some discussion with a more balanced counter point to the deluge of educational material from real estate agents and property spruikers indicating that gearing up to buy property is a road paved with gold.

Our next article in this series will further test this theory by taking a forward-looking approach to determine whether given our expectations around future movements in the property and financial markets, a strategy of buying or renting and investing is likely to prove optimal over the next decade.

Notes

1 – Labour Force, Australia, January 2018 – Australian Bureau of Statistics

2 – An NPV Analysis of Buying versus Renting for Prospective Australian First Home Buyers – D. Crowley & S.M. Li

As investors reflect on re-balancing portfolios and assessing risks, many are understandably eager…

From November, new Australians will face an updated citizenship test answering questions on their knowledge…

Two of the team from Dorado Property have been appointed to the Property Council’s industry committees…

Having spent years building a career in North America, Australian-bred David Giles returned…